If there’s one thing I’ve learned to do well, it’s budgeting. Ever since I was young, I’ve understood the value of knowing where my money goes and how to get the most out of it. That’s why I want to walk you through my budgeting process, so you can learn how to save more and spend more on the things that actually make you happy.

Let me be clear: the goal of budgeting isn’t to live a boring life or to cut costs on everything just to have more money sitting in your bank account. Budgeting is really about making better choices with your money. It’s about dividing your income wisely so you can enjoy life both now and in the future.

Before we get into the details, I should mention that I’m a single person living in Germany. So, the examples I share will mostly reflect that lifestyle and might be more useful if you’re in a similar situation.

Essentials

The first step in budgeting is figuring out your essential expenses. These are the things you need to pay for no matter what, things you simply can’t live without. Here are some examples from my own budget:

- Rent

- Utilities (water, electricity, heating, internet, phone)

- Groceries

- Insurance and taxes

- Self-care

- Transportation

Since these are fixed costs that come up every month, even small savings here can make a big difference over time. That’s why I review my essentials every year to see if I can cut back or switch to better deals.

Let’s go over each of these categories so you can get an idea of how to optimize them. I’ll also share some of my actual numbers to give you a point of reference, especially if your lifestyle is similar to mine.

Rent

In Germany, rent is usually split into two parts: cold rent and warm rent. Cold rent is just for the apartment or house itself. Warm rent includes additional costs like heating, water, and sometimes other shared building expenses.

In many cases, there’s not much you can do to lower your cold rent unless you move to a smaller place, a different neighborhood, or live with a partner or flatmate to share costs.

However, warm rent gives you more room to save. One way I’ve cut costs is by using smart radiator valves, like the ones from Eve. Since I installed them, my heating bill has dropped by about 30%. These devices control the heat more efficiently, so you don’t waste energy. The upfront cost pays for itself in about a year or two, and after that, you’re just saving money.

Utilities

When it comes to utility bills like electricity, internet, and mobile plans, there’s actually a lot you can do to save money. In Germany, most companies use the same infrastructure, so the quality of the service stays the same no matter which provider you choose. This means you can switch providers without losing quality, and often pay much less.

One of the easiest ways to save is by taking advantage of special offers for new customers. Many companies offer lower prices or bonuses during the first year or two of a contract. Websites like CHECK24 can help compare offers, but keep in mind they often only show deals from companies that pay them a commission. Because of this, you might find even cheaper options by looking directly on company websites or using other comparison tools.

When comparing offers, don’t just look at the monthly cost. Some contracts come with bonuses, cashback, or discounts that only show up if you calculate the total cost over the full contract period. Always check how much you’ll pay in total over 12 or 24 months, and use that number to compare.

Once your contract ends, never just continue with the same provider. Prices usually go up after the first contract period. It’s better to switch again and take another new-customer deal. This might sound like extra work, but switching is actually very simple in Germany, especially for electricity, internet, and mobile. Most of it can be done online with no paperwork.

You can also save more by waiting for Black Friday deals. Many companies offer bigger discounts during that time. If you time your contract to start on Black Friday, you can plan to switch again the following year when new deals come around.

I review my contracts every year to make sure I’m not overpaying. Just by doing this, I’ve significantly lowered my internet and phone bills. I also tried switching to an hourly-rate electricity contract to save more, but this year it didn’t work out as expected due to low wind energy. Still, I believe it will be cheaper in the long run.

Here’s what I currently pay:

- Internet: €25/month (100 Mbit/s)

- Electricity: €45/month (80–90 kWh usage, green)

- Mobile: €4/month (3 GB data only)

I only use 3 GB because I don’t stream videos, and I spend just 2–3 hours a day on my phone. I also use FaceTime for calls, so I don’t need a phone or SMS package.

Groceries

One of the biggest money drains in many people’s budgets is ordering food. I can’t stress this enough: ordering food regularly can quickly add up. I’ve seen many of my friends spend a lot of money on food delivery, and it’s not just a small expense. If we look at the order value and revenue of major food delivery companies in 2024, it’s clear how much money is at stake:

- Uber Eats: $74.6 billion / $13.7 billion

- Just Eat Takeaway (parent company of Lieferando): €26.3 billion / €5.09 billion

- DoorDash: $21.3 billion / $2.3 billion

- Delivery Hero: €48.8 billion / €12.8 billion

The top food delivery companies alone are handling over $200 billion worth of orders.

When you order food, you’re paying not only for the meal but also for the delivery, the restaurant’s profit margin, and the app’s commission. In the end, you end up paying a lot more than if you made the meal yourself.

Now, I’m not saying you should never enjoy a meal prepared by a chef, I’ll come back to this later. But the reality is, you have to eat at least two meals a day for the rest of your life. So instead of relying on delivery, there are much cheaper and healthier alternatives.

Here are a few options:

- Frozen Meals: If you’re short on time after work and need something quick, try frozen ready meals. Many people think frozen meals aren’t healthy, but they can actually be a good choice. Unlike other packaged foods, frozen meals don’t use additives for preservation; the cold temperature keeps them fresh. My personal favorite brand is Frosta. They have a wide range of meals that can be heated up in about 7 minutes, and each portion costs between €3–5.

- Cooking for Yourself: If you have a bit more time, cooking your own meals is always a great option. It’s healthier and way cheaper. You may want to invest in kitchen gadgets like a Thermomix, All-in-One Cooker, or Airfryer. These tools can make cooking faster and more efficient, and while the initial cost might seem high, you’ll save money in the long run.

- Buy Store Brands: When you’re grocery shopping, look for the store brands. Most of the time, these products are just as good as the big-name brands but much cheaper. My go-to supermarket is REWE, and I buy their own branded items whenever I can. They’re often on sale, and the quality is surprisingly good. If you want even cheaper options, discount supermarkets like ALDI or PENNY have great store brands as well.

When it comes to my monthly grocery expenses, I spend around €200–250 per month for one person. This includes:

- Two small meals a day (yogurt, muesli, and seasonal fruit)

- One breakfast (eggs, etc.)

- One dinner (chicken or seafood, a side like potatoes or rice, and a salad with seasonal veggies)

Compare that to the cost of ordering food. For example, a Big Mac menu ordered through McDonald’s app costs €12.59 for the food, but with delivery fees and service charges, it’s closer to €15. If you ordered two meals a day, you’d be spending over €1,000 per month. Even if you opt for cheaper fast food, you’re still paying 3–4 times more than if you cooked at home.

When I worked in an office, I noticed how expensive it was to eat out for lunch every day. I’d spend around €10–15 per meal, which added up to nearly €200 a month. But many offices in Germany have microwaves, and a lot of people bring meals from home to heat up. There’s even a Reddit community called Meal Prep Sunday, where people cook for the whole week and store it in the fridge. This way, you just warm it up each day. Since I work from home now, I prefer to cook fresh meals when I’m hungry.

Toiletries

Similar to groceries, I also buy most of my toiletry items from store brands. However, keep in mind that some of these products might not work for everyone, especially if you have skin sensitivities or other specific needs. For example, I’ve used the same shampoo for years, and if I switch, I get skin problems. So, if you do decide to try store brands, make sure they’re right for you.

One trick to save even more is to stock up on toiletries when they’re on sale. These products have a long shelf life, so you can buy in bulk and save money over time, while avoiding the impact of inflation.

Insurance and Taxes

In Germany, there are a few key insurance policies that are highly recommended, particularly liability insurance and household insurance. These are both affordable and provide peace of mind. I use Getsafe and pay about €5 per month for both. Depending on your situation, you might also want to consider dental insurance since regular health insurance doesn’t cover all dental expenses.

Another unavoidable expense in Germany is the Rundfunkbeitrag (broadcasting fee). This is a contribution to the public broadcasting system and costs €18.36 per month per household. There’s no way around this, so it’s something to factor into your monthly budget.

Self-care

Self-care is essential, but it can vary greatly from person to person, making it hard to set a fixed budget. For example, this category can include things like haircuts, cosmetic products, and other personal care items.

For me, self-care expenses are minimal because I don’t use many cosmetic products. When I do buy something like sunscreen, deodorant, etc. I include it in my grocery budget.

When it comes to haircuts, during the COVID pandemic, I learned how to cut my own hair. I invested in some tools to help me, and now I cut my hair at home. If you think you could manage this, I highly recommend it. Haircuts are something we all need regularly, and by doing it yourself, you can save a lot of money over the years. If you or your partner can learn to cut hair, that’s a skill that pays off in the long run.

Transportation

I don’t own a car, and I have no plans to get one. I believe owning a car is expensive, and I’m lucky to live in Hamburg, a city with great public transportation. I could pay €58 per month for the Deutschlandticket, which gives me unlimited access to public transport.

That said, I don’t use public transport much because the city has very good cycling infrastructure. A couple of years ago, I bought an e-bike, and now I use it for almost all my transportation needs. So, my transportation costs are practically zero.

If you live in a city with great public or cycling infrastructure, I highly recommend you skip owning a car. If you need a car occasionally, consider using MILES or other car rental services for those rare occasions.

Non-essentials

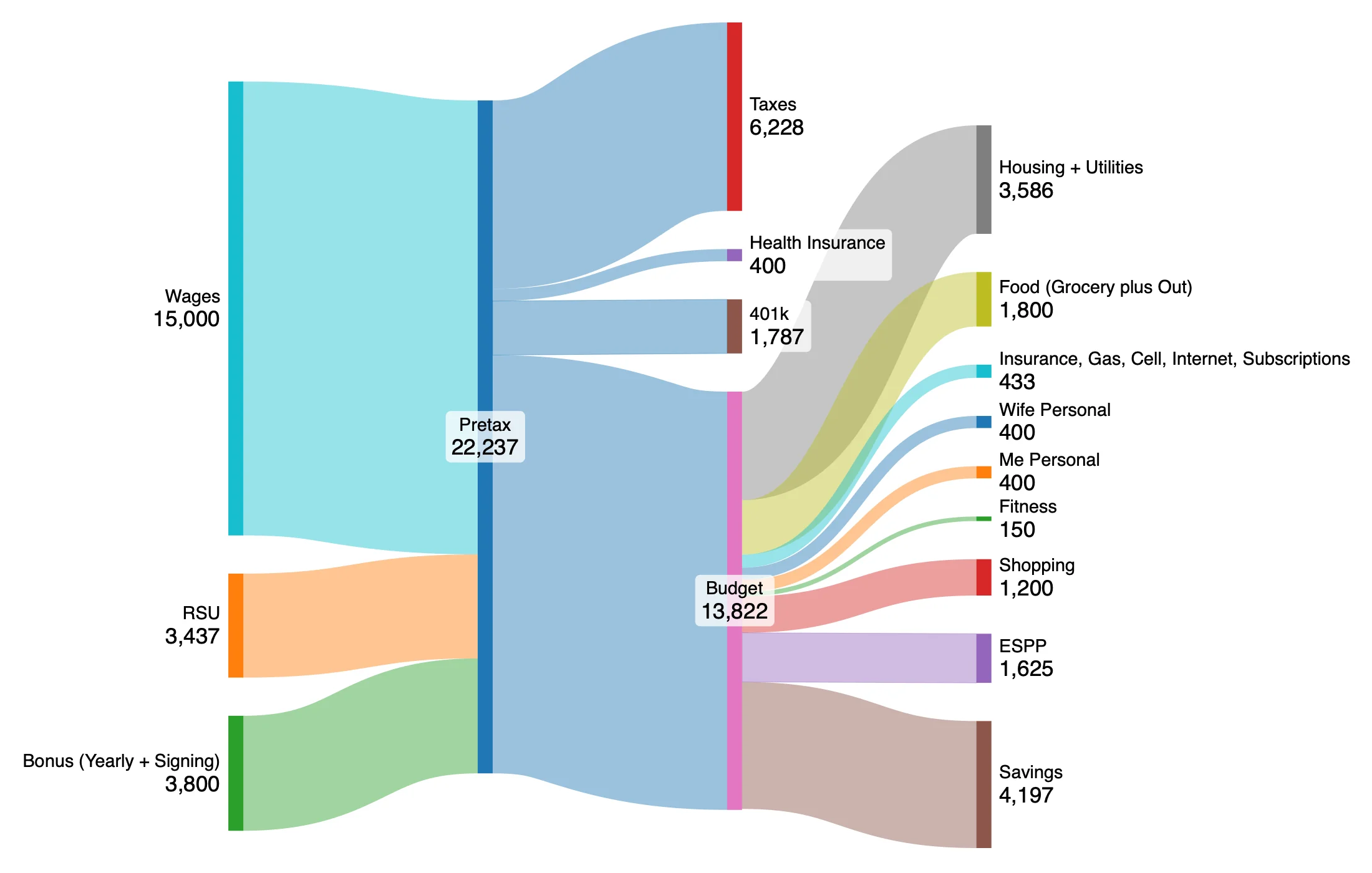

This is probably the most fun part of budgeting. Once you’ve followed the advice I’ve shared and saved money on your essentials, you’ll have a bigger budget to spend on things you enjoy. But before diving into the different categories, I want to mention one important thing: savings.

What helps me spend money without stress is having a clear savings plan. In Germany, the average savings rate is around 10%. However, this varies depending on your goals—whether you want to build a retirement fund or maybe even retire early. I’ve written more about this in a different post, so I won’t go into detail here. I just want to emphasize that setting aside some money each month is crucial. It’s not just for the future; it also gives you peace of mind now, knowing you’re financially secure.

For me, once my essential expenses and savings are sorted, I know exactly how much I have left for the non-essential stuff. I get my salary, set aside the amount for essentials, send the money I want to invest to my broker, and then I’m left with the rest to spend freely.

Eating Out

I give myself a bit more flexibility in the eating out category since I save money by cooking most of my meals at home. Going out for a meal with friends is a treat, and I don’t stress too much about the cost. Typically, a café visit with coffee and cake costs around €10, while a meal at a restaurant averages €15–20. For special occasions, I might splurge on a slightly pricier restaurant, but even then, I rarely spend more than €35.

Since I only eat out 7-8 times a month, it’s hard to spend more than €150 on eating out. This makes it a manageable and enjoyable category for me.

Vacation

Vacation is one of the non-essential categories where I recommend setting a budget, just like you would for savings. The key is to plan ahead and save regularly, so you’re ready when it’s time to go.

Most people don’t take vacations every month, but there are likely a few times during the year when you want to go away for a week or two, plus maybe a couple of weekend trips. To make this possible, set aside a bit of money each month for your vacation fund. The amount you save will depend on how often you go on vacation and how much you typically spend.

Here’s how to do it: Estimate how much you usually spend on vacations throughout the year. Once you have that number, divide it by 12 (for the 12 months in a year) and save that amount each month. To keep the money separate from your daily spending, I recommend using a neobank like N26, which has a feature that lets you create separate saving spaces. This helps you avoid accidentally spending your vacation money on other things.

The key tip here is to plan your vacation a few months in advance. By doing so, you can score cheaper deals on flights and hotels. These are often the biggest expenses of your vacation, and by saving money there, you’ll have more left over for things like dining out, museums, or activities.

Also, don’t forget to look for seasonal discounts. Hotels and airlines often offer discounts in the opposite season. For example, many summer deals are available in the winter months, and winter deals can be found during the summer. If you don’t have kids, consider booking during school periods (before or after holidays) to find cheaper prices, as that’s when fewer families travel.

Shopping

Some people may consider shopping as an essential, especially for things like clothing or household items. However, I include it in my non-essential budget. Typically, you already have what you need, and the desire to buy something new comes when things wear out. While I understand that some people want to buy new things constantly, I don’t find that sustainable.

My approach is simple: I focus on buying items that last longer, rather than purchasing a lot of cheap things. For clothing, I prefer UNIQLO; for sports gear, I go to DECATHLON; and for electronics, I stick to well-known brands like Apple.

If I’m saving for something big—like a new device or a piece of furniture—I follow the same method I use for vacations: I save a little each month until I’ve reached the amount I need to buy it. If an unexpected need arises, like a broken phone, I tap into my emergency fund and then replenish it by saving a bit each month.

Leisure

Leisure spending can vary a lot depending on your interests. For some, it includes streaming services, gym memberships, or going to concerts/cinema. Personally, I don’t have a gym membership; I prefer exercising at home or in the park unless I’m going bouldering with friends.

When it comes to streaming, I avoid juggling multiple subscriptions. Instead, I cancel one after I’ve finished watching, then switch to another when I’m ready for something new. This keeps things interesting, and by the time I return to a service, there are usually plenty of new shows to catch up on.

The biggest part of my leisure budget goes to books. I buy a lot of them, but I always try to shop second-hand on sites like medimops to save money.

The key here is setting a clear leisure budget. It’s easy to overspend on things you enjoy, so having a spending limit ensures you don’t go overboard. Another way to stay on track is to plan your activities in advance. For example, if you love concerts or festivals, set a goal of attending like 4 per year. If you’re into video games, you might decide on buying 4 AAA games and 3 indie games each year.

Conclusion

I hope you found this post helpful! As I mentioned at the start, the goal here is to share how I approach budgeting. I focus on saving money in areas I don’t mind, like cooking at home or buying supermarket brands, so I can spend more on things I truly enjoy, like eating out, buying books, and traveling.

Of course, your priorities might be different, but the key takeaway is this: you need to save in some categories to enjoy more in others. It’s all about finding a balance that works for you and making sure your spending aligns with what brings you joy.